The Micro, Small, and Medium Enterprises (MSME) segment is booming and is touted to be the growth engine for the economy.

However, the availability of credit remains a key challenge.

The Government, through various schemes and incentives, along with initiatives from the banking industry, has strived to help MSMEs grow multifold in the recent decade.

Still, it isn’t fulfilling the demand for credit amongst MSMEs and is holding back the potential employment opportunities that can be created across the country. The Standing Committee on Finance (chair: Jayant Sinha) in 2022 noted a credit gap of INR 20-25 lakh crore. With over 63 million MSMEs in the country adding to over 30% of the GDP and supporting 110 million employees, there is a need for a robust platform to provide credit.

That’s where OCEN comes in.

The Open Credit Enablement Network (OCEN) is a transformative initiative that’s changing the financial landscape of India.

In this deep-dive on OCEN, we have covered:

- What is OCEN

- How does OCEN work

- How OCEN aims to transform the Indian economy

- Real-world examples of OCEN

What Is OCEN?

OCEN is an open protocol designed to democratise access to credit in India. Launched by the Indian government in collaboration with several private sector stakeholders, OCEN aims to create a simplified platform for credit dissemination by onboarding lenders, borrowers, and intermediaries like loan agents/aggregators and technology service providers and allowing them to interact seamlessly to extend credit. It’s akin to the Unified Payments Interface (UPI) but for the lending ecosystem, fostering a more inclusive, efficient, and transparent credit market.

The rationale behind OCEN

Traditional lending mechanisms in India can be cumbersome and inefficient, especially for small and medium enterprises (SMEs) and individual borrowers.

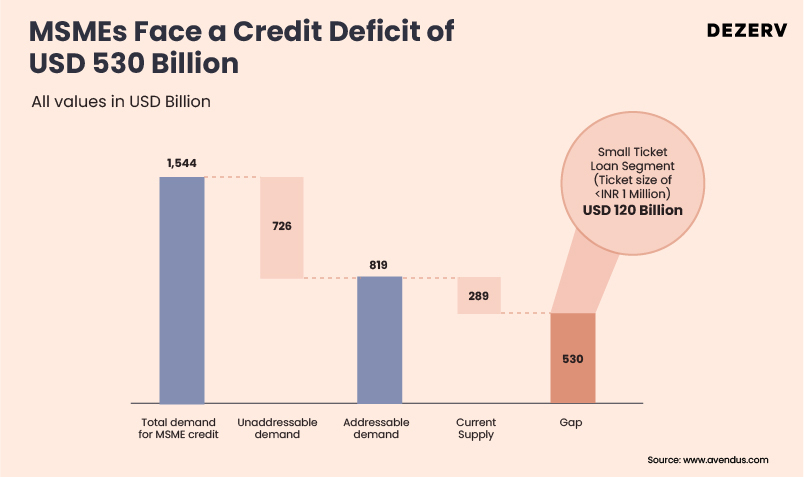

According to Avendus, the MSME sector faces a significant obstacle with a credit gap exceeding USD 500 billion, including over USD 100 billion in the small-ticket loan segment.

Lending institutions often avoid the short-term working capital requirements of MSMEs owing to the cost of customer acquisition, loan processing, compliance, and the overall cost of managing the operations versus the interest spread generated from lending. The difficulty in addressing these issues has led conventional lenders to avoid such lending options.

“India needs to go that extra mile in offering credit to the most deserving, smallest businesses and individuals. With most credit directed to large companies in large volumes, smaller companies and micro enterprises are left in the lurch with little or no access to credit at all, which is a huge concern for the next growth phase of the industry,” said Nandan Nilekani, co-founder of Infosys and former chairman of the Unique Identification Authority of India (UIDAI), at the Global FinTech Festival, 2020.

By standardising the credit application process and creating a more accessible credit market, OCEN seeks to bridge this significant gap and empower millions of underserved individuals and businesses.

How does OCEN work?

OCEN functions as an open architecture framework that allows various players in the lending ecosystem to interact seamlessly.

Here’s a breakdown of its key components:

- Standardised APIs: OCEN provides a set of standardised Application Programming Interfaces (APIs) that enable different entities to communicate effectively. These APIs facilitate data sharing, credit assessment, loan disbursal, and repayment processes.

- LAs (Loan Agents): In their simplest form, LAs are a loan marketplace that enables borrowers to compare loan offers from multiple lenders and choose the best one. In a more advanced version, the LAs are akin to a borrower’s financial advisor, looking after their interests, fetching the best offers and advising the customer to make good decisions.

- Lenders: Banks, non-banking financial companies (NBFCs), and fintech firms integrate with OCEN to access a broader borrower base. They benefit from more efficient underwriting processes and lower operational costs.

- Account Aggregators (AAs): These entities play a crucial role in the OCEN ecosystem by aggregating financial information from various sources (with users’ consent) to provide a comprehensive credit profile for borrowers.

Benefits of OCEN

1. Inclusive access

Credit availability to MSMEs in India remains significantly lower than global averages. While scheduled commercial banks have traditionally led in meeting credit needs, we are now witnessing an increasing number of innovative, technology-driven players transforming the digital lending landscape.

Though still in its early stages compared to traditional lending, digital lending is expanding at a remarkable pace, with total disbursements expected to exceed INR 47.4 lakh crore by 2026. OCEN is expected to contribute significantly towards this growth.

One of OCEN’s primary goals is to democratise access to credit. By leveraging digital platforms, it brings credit facilities to previously underserved segments of the population, including small business owners, gig economy workers, and rural entrepreneurs.

2. Efficiency

OCEN significantly reduces the time and cost associated with credit disbursal. Traditional loan processes, often marred by paperwork and manual verifications, can take weeks or even months. In contrast, OCEN facilitates seamless interaction between lenders, borrowers, and Loan Agents (LAs) at scale, which means that OCEN-enabled digital lending platforms can process loans within hours.

3. Transparency

By promoting standardised credit protocols, OCEN enhances transparency in the lending process. Borrowers receive clear and consistent information about loan terms, interest rates, and repayment schedules. This transparency fosters trust and encourages more individuals and businesses to seek formal credit.

4. Customised credit products

OCEN’s integration with various digital platforms allows for the creation of customised credit products. Lenders can tailor their offerings based on the specific needs and financial behaviours of borrowers.

The impact on India’s financial ecosystem

Enhancing competition

OCEN opens up the lending market to a broader range of players, fostering innovation and competition. Traditional banks, NBFCs, and fintech firms can compete on a level playing field, driving better credit terms and lower interest rates for borrowers. This increased competition will benefit businesses, making credit more affordable and accessible.

Supporting economic growth

During the release of the OCEN 4.0 the team behind developing OCEN mentioned that lending institutions have used past GST data to assess the revenue growth and extend credit accordingly. However, this has helped only 14% of MSMEs to access credit as per their requirement the balance 86% have not been able to access credit as per their requirement. OCEN intends to support such MSMEs in allowing them to present their borrowing and repaying capabilities properly and secure credit to their short term requirements. This will particularly help individuals and businesses in rural and semi-urban areas, where traditional banking infrastructure is often limited.

Real-world examples of OCEN in action

Several pilot projects and implementations have demonstrated OCEN’s potential:

E-commerce platforms:

E-commerce giants like Amazon and Flipkart have integrated OCEN to provide working capital loans to their sellers. By analysing sales data and transaction histories, these platforms offer customised credit products with quick approval and disbursal.

Gig economy platforms:

Ride-hailing and food delivery platforms have used OCEN to extend personal loans to their drivers and delivery partners. These loans are based on the workers’ earnings and job stability, providing them with much-needed financial support.

Payment gateways:

Payment gateways have utilised OCEN to offer credit products to small businesses using their services. These loans help businesses manage cash flow and invest in growth opportunities.

In summary

As someone deeply involved in the financial sector, I have witnessed the transformative potential of digital innovation. The introduction of OCEN is a significant milestone in India’s financial journey. By breaking down barriers and fostering a more inclusive credit ecosystem, OCEN empowers individuals and businesses, driving economic growth and prosperity.

I recall a conversation with a 20-year-old entrepreneur who, despite having a thriving online business, struggled to secure a loan due to a lack of collateral. With OCEN, such entrepreneurs can now access credit based on their digital footprints and transaction histories without the need for traditional collateral. This shift not only supports individual growth but also contributes to the broader economic development of our country.

I’m quite excited to see how OCEN develops and adapts to evolving market requirements.