The biggest problem impacting wealth creation is the lack of a holistic view of all investments. Over time, as portfolios expand, affluent investors are unable to monitor and adapt their portfolios to changing market conditions. The biggest reason is the absence of a single place to view all investments and their performance.

Launched in 2021, RBI’s Account Aggregator (AA) Framework aims to solve this very problem for wealth creators.

Account Aggregators (AAs) are touted to be a game-changing solution by addressing persistent issues in the digital sharing of financial data, and that is what I will talk about today.

In this blog, we will explore:

- What are Account Aggregators, and how do they work?

- How the AA framework is transforming financial management

- Use cases of AA

- How AA can be leveraged for wealth creation

What are Account Aggregators (AA)?

Account Aggregators, introduced as a new class of regulated entities and categorised under Non-Banking Financial Companies (NBFCs), became functional in 2021.

Their primary role is to facilitate the secure and consent-based transfer of financial data between Financial Information Providers (FIPs) and Financial Information Users (FIUs), ensuring a smooth interaction between institutions like banks and lenders.

This framework offers a comprehensive view of your finances, simplifies expense tracking, and facilitates access to personalised financial services. AAs promise to make financial transactions simpler, faster, and more secure for everyone with you in charge of your data.

The key is that your data is never shared without your permission. Instead of collecting all your financial data in one place, Account Aggregators act as “consent managers.” This means they control who can access your information and only allow it after your go-ahead.

The Account Aggregator (AA) network connects 400 financial institutions across four major regulatory bodies:

- The Reserve Bank of India (RBI)

- The Securities & Exchange Board of India (SEBI)

- The Insurance Regulatory & Development Authority of India (IRDAI)

- The Pension Fund Regulatory & Development Authority (PFRDA).

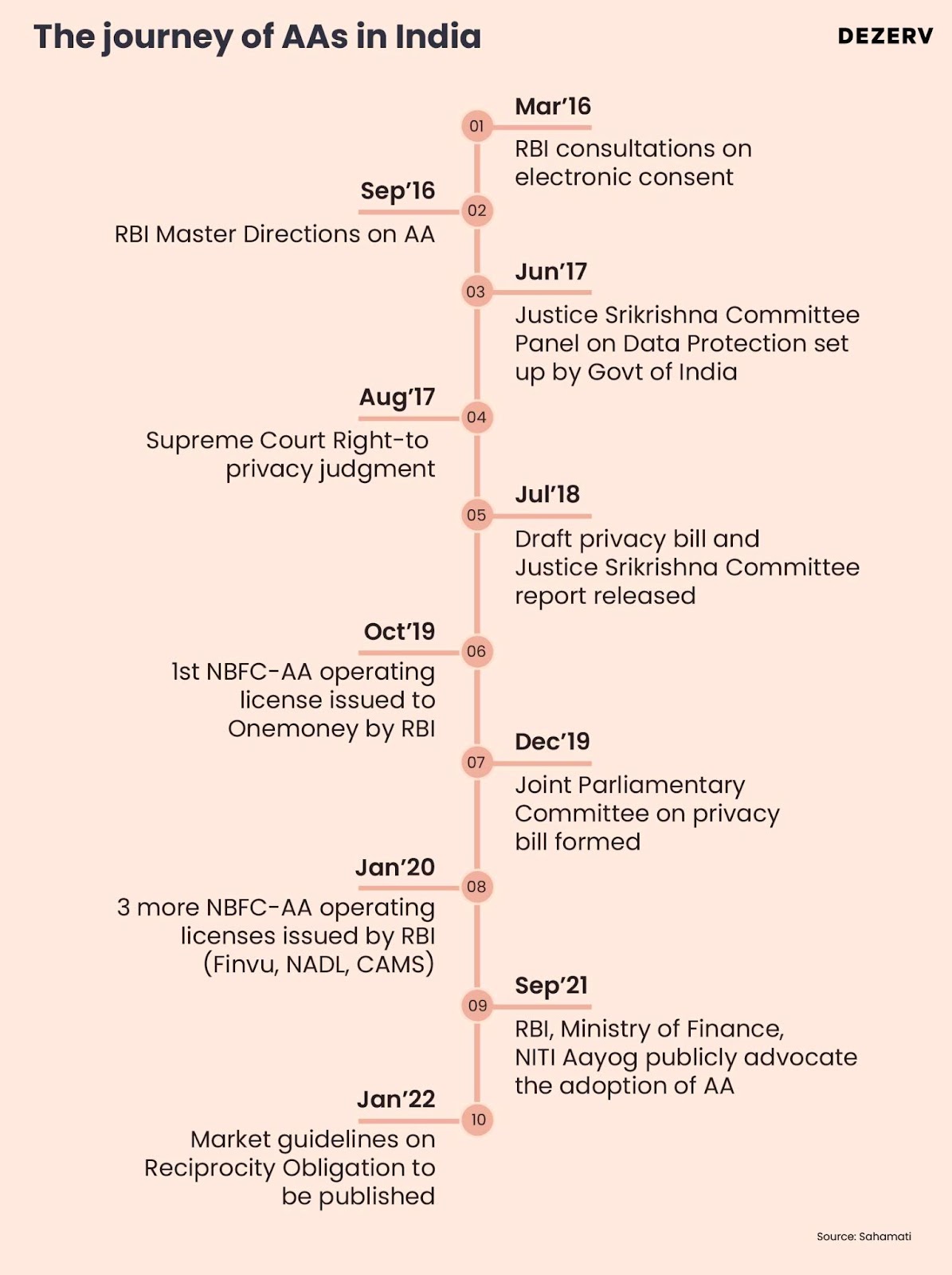

The journey of AAs in India

How does the Account Aggregator system work?

There are 4 major segments of the AA system:

- Financial Information Provider (FIP): Financial Information Providers (FIPs) hold and manage user data.

These include banks (such as HDFC Bank, Axis Bank, etc.), NBFCs (such as LIC Housing Finance Ltd, Bajaj Finance Ltd, etc.), depositories (such as the Central Depository Securities Limited and the National Securities Depository Limited) and asset management companies.

FIPs provide user data to Financial Information Users (FIUs), which are other institutions or services that need this data to operate. - Financial Information User (FIU): A Financial Information User (FIU) is an entity registered with a financial sector regulator that uses data from FIPs to offer services to customers.

For example, if a person wishes to take a loan and the bank has to ascertain and verify the creditworthiness of the applicant, the bank will connect with FIPs and act as an FIU by accessing data from other banks or financial institutions.

- Technology Service Provider (TSP): Technology Service Providers (TSPs) work with FIUs and FIPs to create products and services for Account Aggregators.

TSPs build the core technology and infrastructure that supports the Account Aggregator system. Some popular examples are PhonePe, Setu, CAMS, Kfin Technologies, etc.

- Certifiers: Certifiers ensure that everyone in the Account Aggregator system follows the technical rules set by ReBIT.

Account Aggregators (AAs) do not view or store your financial data; they simply transfer it between institutions based on your permission.

Despite their name, AAs don’t “aggregate” or compile your data like the tech companies. Instead, the data they handle is encrypted by the sending institution and can only be decrypted by the receiving institution.

End-to-end encryption and digital signatures make sharing information through AAs much more secure than sending paper documents.

How is the AA framework making financial management easy?

- For individuals: Account Aggregators are transforming the world of fintech by making it easier to access financial information. This leads to more personalised services and greater convenience for individuals.

- Streamlined financial management by consolidating scattered data across banks, credit cards, loans, investments, and insurance policies into one convenient platform.

- Time and effort saving via access to all account balances and transactions through a single login, eliminating the need to log in across multiple accounts.

- Empowering individuals with insights into their financial health enables better decision-making and future planning.

- Streamlined financial management by consolidating scattered data across banks, credit cards, loans, investments, and insurance policies into one convenient platform.

- For businesses: Account aggregators help businesses boost sales by allowing them to offer customised products that match customer needs. It lets companies quickly confirm user identities, reducing fraud risk and speeding up customer onboarding.

Some advantages of the AA framework for businesses and MSMEs:

- Using data aggregator software saves businesses time and money by accessing verified data, speeding up onboarding processes, and meeting compliance requirements like ID verification.

- Aggregators help lenders make better decisions by providing detailed information about loan applicants, making lending fairer and increasing the chances of more people getting approved for loans.

- Sharing verified data opens up new opportunities for online insurers and lenders in places like India, making reaching more customers easier and expanding their market.

- Account Aggregators make it easier for lenders to assess creditworthiness quickly and accurately, helping non-bank financial companies (NBFCs) compete with banks and process more loan applications.

- Aggregating financial accounts allows businesses to offer personalised services, leading to more sales and happier customers by giving them a clearer picture of their finances.

- Using data aggregator software saves businesses time and money by accessing verified data, speeding up onboarding processes, and meeting compliance requirements like ID verification.

- For financial institutions: Account Aggregators streamline the identity verification process for financial institutions by replacing manual analysis of bank statements. This reduces errors and offers a more accurate picture of a customer’s finances.

Moreover, AAs lower transaction costs by providing reliable data, which helps reduce underwriting expenses and boosts loan approval rates.

Use cases of the AA framework

- Lending: In modern lending, borrowers typically provide banking information via hard copies or PDFs, leading to inefficient processing and security concerns.

Account Aggregators (AAs) offer a transformative solution by enabling lenders to access real-time, digitally signed data directly from FIPs. This streamlined process expedites lending, reduces risk, and allows for tailored loan products while facilitating uninterrupted loan monitoring for lenders.

- Personal financial management: In India, personal finance management (PFM) app usage remains low due to inadequate financial knowledge and concerns about data security. Current methods of accessing bank statements, such as uploading PDFs or sharing login credentials, are inefficient and compromise privacy.

PFM apps are crucial in empowering individuals to make informed financial decisions, necessitating actionable reports and user-friendly data visualisation features for enhanced usability and effectiveness. - Wealth management: Wealth managers often rely on clients to provide financial data, which can be inefficient. Account Aggregators offer a solution by allowing clients to authorise data sharing directly with their wealth manager, eliminating the need for sharing login credentials.

This streamlines the process, enhances data security, and enables wealth managers to generate actionable insights efficiently. Wealth managers can thus expand their client base and improve operational efficiency by leveraging technology and Account Aggregators.

Overcoming the challenges of AA

One major challenge is getting all stakeholders across various regulatory frameworks to participate in the same protocol and quality. The objective should be to be as frictionless and open as UPI to ensure final user adoption.

The RBI has laid the groundwork for the system by first establishing a regulatory framework and then setting forth the technical standards. It should feature a proper consent architecture and maintain audit trails. The guidelines require FIPs to implement interfaces that allow an Account Aggregator to submit consent artefacts and authenticate each other, enabling the secure flow of financial information to the Account Aggregator.

Account Aggregators face significant challenges in safeguarding the security and privacy of users’ financial data. The potential risk of unauthorised access by hackers, which could compromise sensitive personal and financial information, is a major concern.

The Reserve Bank of India (RBI) is instituting robust measures to ensure data integrity. These include the deployment of end-to-end encryption and the use of secure digital signatures for data sharing. Additionally, integrating advanced technologies, such as artificial intelligence (AI), further enhances the platform’s security.

How does the AA framework affect you?

AA simplifies financial planning and portfolio management by consolidating information from multiple accounts. For example, individuals can securely share their bank account details, investments, and insurance policies, enabling more informed advice based on a holistic understanding of their financial situation.

AA can also shift lending from asset-backed to cash-flow-based, opening doors for people and small businesses that have traditionally been overlooked by banks.

In May 2024, CAMS, one of India’s largest Registrar and Transfer agencies, started leveraging granular data through the AA framework to strengthen their offerings in mutual fund investing, PFM and lending.

At Dezerv, we are leveraging AA to transform the investing experience for investors.

Dezerv is empanelled as an FIU with Sahamati AA and is in the final stages of its integration.

In the next few weeks, we will allow all our users to track their stocks and ETF investments on Dezerv’s Wealth Monitor with the ability to add savings accounts tracking and expense analysis.

In summary

AA is reshaping India’s financial landscape by empowering individuals and businesses with greater control over their financial data. Since its launch in 2021, the AA system has made significant strides, with over 1.94 billion now AA-enabled and 40.09 million users leveraging this platform to share financial data with banks and other institutions. This shift towards a consent-based model ensures security while offering faster, more efficient access to loans and other financial services.

The future looks promising with the government’s plans to establish a National Financial Information Registry (NFIR) as part of the 2023-24 budget. Once connected to the AA network, this registry could further facilitate credit access and streamline financial services for the underserved. The Account Aggregator system, in partnership with regulatory bodies and financial institutions, is not just a leap toward technological advancement—it’s a stride toward a more inclusive and accessible financial ecosystem in India.

Disclaimer: The information contained herein is for informational purposes and should not be interpreted as soliciting, advertising, or providing any advice.